Using the equity from your home can provide you with cash at a relatively low interest rate to fund big life events and financial strategies including home improvements, advanced education, debt consolidation, paying unexpected bills, or bridging expenses in retirement. In any of these cases, having a solid understanding of how you can draw on your home equity using either a home equity loan (HELOAN) or a line of credit (HELOC) is important.

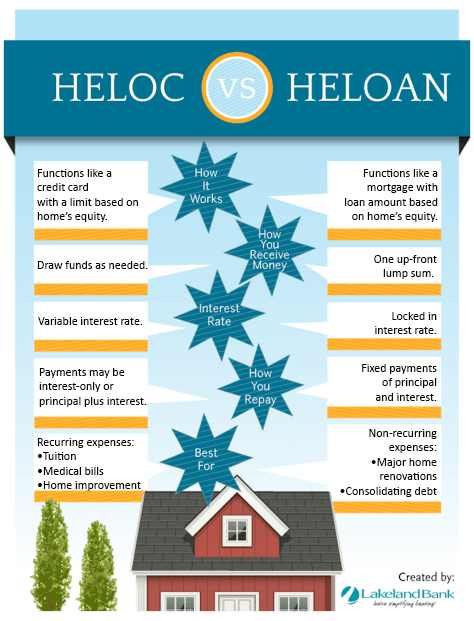

HELOANs typically have fixed interest rates and are amortized over a term that can range between five and 20 years. Consumers receive a lump sum (or full proceeds) as opposed to taking gradual advances with a HELOC. Since the interest rate is fixed, the monthly payment won’t fluctuate as interest rates change.

HELOCs generally have a variable interest rate based on the prime rate plus a margin. You are able to borrow varying amounts against your line of credit during the draw period which is typically between five and 10 years. After that, the outstanding balance may amortize over a period that generally ranges from 10 to 20 years.

Depending on what you use the loan proceeds for and, if your deductions are higher than the standard deduction, the interest on these types of loans may be deductible (we advise you to check with your tax professional).

As you figure out your financial plan, consider how much you want to borrow, whether this is a one-time need or for multiple expenses, and how soon you’ll be able to pay down the balance. You also want to ensure your ability to make the monthly payments so you don’t put your home at risk.

Here are some reasons to use either a HELOAN or HELOC to borrow against your home equity:

Home Improvements - Major repairs and renovations can be costly. If you don’t have sufficient savings, using your home equity may be a great way to finance these, especially if the changes add to the value of your house. Make sure that you have the funds to pay off the balance by budgeting for this extra expense.

New Car - If you’re in need of a new car, your home equity loan can provide you with low-cost funds. Before borrowing against the equity in your home, compare interest rates and terms for a home equity loan with a traditional auto loan.

Consolidate Credit Card Debt – Traditionally, credit cards have much higher interest rates than home equity loans, and you can use a home equity loan to consolidate debt. While you will pay less interest that may allow you to pay down this debt sooner, it’s crucial that you budget carefully for this loan payment since missing payments could put your home at risk.

College Tuition - Your home equity may provide a lower interest rate than some student loans, which could be used to pay off the student loan. If you’re nearing retirement, you may want to reconsider using these funds for college education if this loan will interfere with your financial plans. Also, if you use home equity to fund a child’s tuition in lieu of a traditional student loan, you will be the one responsible for this debt rather than your child.

HELOC or HELOAN?

Which option is best for you? The infographic below discusses some of the most significant differences between HELOCs and HELs.

We’re here to help! You can find more information about this topic and others in our Simply Speaking blog. And, our Customer Service Team can be reached at 866-224-1379.